As the old saying goes, “failing to plan is planning to fail.” If you are setting your sights on the exhilarating world of entrepreneurship, there’s no avoiding the nitty-gritty of financial planning. Startup costs form the bedrock of your venture and accurately estimating them is akin to building a solid foundation for your business castle.

Contents

Understanding Business Startup Costs

Before going into the particulars of estimating startup costs, it’s essential to grasp what these costs encompass and why they are so crucial to your business plan. Understanding these costs is the first step toward effective financial planning and setting your business up for success.

Define Business Startup Costs

Business startup costs are the expenses incurred during the process of creating and setting up your new business. These costs can range from purchasing equipment and inventory to legal fees and licenses. Essentially, these are the initial investments you make to get your business off the ground before it begins generating revenue.

Explain the Role of Startup Costs in Business Planning

Now that we have defined what startup costs are, let’s talk about their role in business planning. Startup costs are more than just numbers on a paper; they are the blueprint for your business’s financial health.

- Assessing Feasibility: By estimating these costs, you can assess whether your business idea is financially viable. If the estimated costs are too high, it might be an indicator that your idea needs reworking or reconsidering.

- Securing Funding: When you approach investors or apply for loans, the first thing they want to see is your financial plan. A well-estimated and detailed breakdown of your startup costs can make the difference in securing the funding you need.

- Allocating Resources Wisely: Understanding your startup costs allows you to allocate your resources efficiently. Knowing where each dollar is going helps in prioritizing expenditures that are essential for your business’s growth.

- Mitigating Risks: A comprehensive understanding of startup costs aids in foreseeing potential financial challenges. This awareness allows you to develop strategies to mitigate risks associated with unexpected expenses.

Differentiate Between One-Time and Ongoing Costs

When considering startup costs, it’s crucial to understand that not all expenses are the same. Generally, these costs can be broken down into one-time costs and ongoing costs [1].

One-Time Costs

These are expenses that you only have to pay once, such as purchasing equipment, initial marketing campaigns, and setup fees for utilities or services. These costs are typically upfront and are essential in establishing your business operations.

Ongoing Costs

Ongoing costs are recurring expenses necessary to keep your business running. These include rent, utility bills, employee salaries, and inventory replenishment. Planning for ongoing costs is just as crucial as one-time costs, as they will impact your business’s ability to maintain operations in the long term.

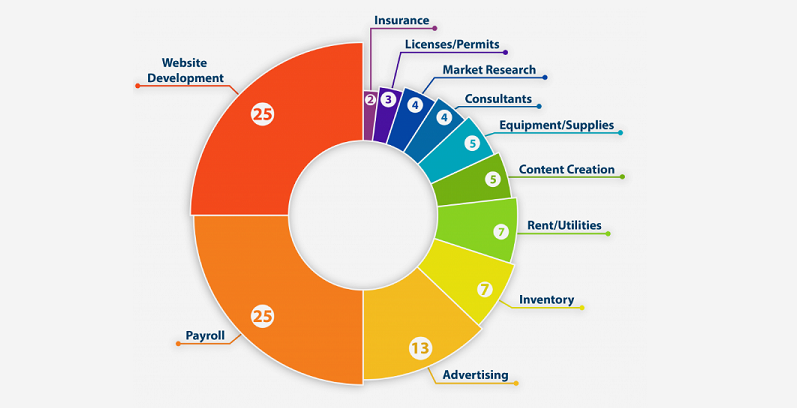

Essential Components of Business Startup Costs

With a clear understanding of what business startup costs are and their importance in business planning, it’s time to dive into the various components that constitute these costs. Identifying and evaluating each element is crucial to estimating your startup costs effectively. Here’s a breakdown of the essential components you’ll need to consider:

Inventory and Initial Stock

Whether you’re starting a retail store, a restaurant, or an e-commerce website, you will need inventory. This encompasses the products you’ll be selling or the raw materials needed to create them.

- Bulk Purchases: Sometimes buying in bulk can save money in the long term, but be cautious not to over-purchase.

- Suppliers and Wholesale Prices: Research various suppliers and negotiate wholesale prices to minimize costs.

- Storage Costs: Don’t forget to account for the cost of storing your inventory, especially if you need a warehouse or climate-controlled space.

Equipment and Supplies

Every business needs tools and equipment to operate. This category includes everything from manufacturing equipment to office supplies [2].

- Essential vs. Non-Essential: Prioritize buying essential equipment that directly impacts your business operations.

- New vs. Used Equipment: Assess whether buying used equipment is a viable option to save on costs.

- Maintenance and Upgrades: Keep in mind that equipment will need maintenance, and budget for these future costs.

Legal Fees and Licenses

Starting a business involves navigating legal requirements, which comes with associated costs.

- Business Structure: Setting up your business as an LLC, corporation, or sole proprietorship has different legal and financial implications.

- Licenses and Permits: Factor in the costs for any licenses or permits that your business needs to operate legally.

- Legal Consultation: Allocate funds for consulting a lawyer to ensure your business complies with local regulations.

Insurance

Insurance is a safety net that can protect your business from unforeseen circumstances [3].

- General Liability Insurance: Protects your business from financial loss resulting from claims of injury or damages.

- Property Insurance: If you own the space where your business operates, property insurance is crucial.

- Workers’ Compensation: If you have employees, you’ll need to account for workers’ compensation insurance.

Location and Lease Expenses

If your business requires a physical location, this will be one of your most significant expenses.

- Lease vs. Purchase: Weigh the pros and cons of leasing versus purchasing a property.

- Utility Costs: Consider the costs of electricity, water, and other utilities.

- Renovation and Furnishing: Factor in the costs to make the space suitable for your business.

Branding and Marketing Materials

Establishing a brand identity is vital to make your business stand out.

- Logo and Branding Materials: Invest in creating a professional logo and other branding materials.

- Website: Factor in the costs of building and maintaining a website.

- Marketing Campaigns: Allocate a budget for initial marketing campaigns to promote your business.

Technology and Software

In the digital age, technology is often at the heart of business operations.

- Software Licenses: Account for the costs of software licenses your business will need.

- Hardware: Include expenses for computers, servers, and other hardware.

- Cybersecurity: Allocate budget for protecting your business’s digital assets.

Employee Salaries and Benefits

If you are hiring staff, you’ll need to account for salaries and benefits.

- Salaries: Estimate the salaries you will pay to your employees.

- Benefits: Factor in the costs of health insurance, retirement plans, and other employee benefits.

Contingency Fund

Finally, it’s always wise to have a contingency fund for unexpected expenses.

- Emergency Funds: Set aside money to cover unforeseen costs or challenges.

- Financial Cushion: Having a financial cushion can also help during initial months when revenues might be lower than expected.

Research Methods for Estimating Business Costs

Now that we have examined the essential components of startup costs, the next critical step is to accurately estimate these expenses. Relying on guesswork or vague assumptions can be detrimental to your business. Hence, employing research methods to gather data and make informed estimations is pivotal.

Utilize Industry Benchmarks

One of the most reliable ways to estimate your startup costs is by looking at industry benchmarks. These benchmarks can provide you with averages and ranges for various expenses within your specific industry [4].

- Industry Reports and Studies: Seek out reports and studies that focus on financial data within your industry.

- Trade Associations: Engage with trade associations which often have valuable information and resources regarding costs.

- Business Ratios: Examine industry-specific ratios, such as the average rent per square foot or average marketing spend as a percentage of revenue, to help estimate costs.

Consult Professionals and Mentors

Getting insights from those who have already tread the path can be incredibly valuable.

- Business Mentors and Advisors: Consult with experienced business mentors or advisors who can provide insights and advice based on their experience.

- Professional Consultants: Consider hiring professional consultants who specialize in business planning and financial analysis.

- Networking Events: Attend industry networking events to connect with fellow entrepreneurs and professionals who can share their experiences and insights.

Survey Competitor Expenses

While it may not always be easy to get detailed financial data from competitors, you can still glean valuable information through careful observation and analysis.

- Competitor Offerings and Pricing: Evaluate the pricing and offerings of competitors to infer their cost structure.

- Online Research: Conduct online research to find any available data or information about competitor expenses.

- Customer Surveys: Through customer surveys, you can gather data on what consumers are willing to pay for certain products or services, which can help infer competitors’ pricing strategies.

Leverage Online Tools and Calculators

In the digital age, there are countless tools and resources available online that can simplify the process of estimating startup costs [5].

- Startup Cost Calculators: Use online calculators designed specifically for estimating business startup costs.

- Budgeting Tools: Leverage budgeting tools that allow you to input various expenses and see how they impact your overall financial plan.

- Industry-Specific Tools: Seek out tools that are tailored to your specific industry, as these may provide more accurate estimates.

Creating a Realistic Business Budget

Having thoroughly researched and estimated your startup costs, it’s time to bring all this information together to create a realistic budget. This budget serves as your financial roadmap, guiding you through the initial phase of your business and helping ensure that you make sound financial decisions.

Collate Your Estimated Costs

Begin by collating all the estimated costs you have gathered through research. Organize these costs into categories, such as inventory, equipment, legal fees, etc. This step will give you a clear picture of where your money needs to be allocated.

- Use Spreadsheets: Utilize spreadsheet software to list and categorize all your estimated costs.

- Prioritize Essential Costs: Mark the costs that are absolutely essential for starting your business.

Forecast Your Revenue

While it’s important to know what your expenses are, it’s equally crucial to have an estimate of the revenue your business will generate. This will allow you to gauge whether your business is financially viable.

- Market Research: Use market research to estimate the demand for your product or service.

- Sales Projections: Create sales projections for the first few months or year of your business.

- Be Conservative: It’s wise to be conservative in your revenue forecasts to account for unforeseen challenges.

Balance Costs with Available Funds

Now, compare the total estimated costs against your available funds, including capital investments, loans, or grants. This step is crucial to determine if you have enough funds to cover all your startup costs.

- Funding Gap Analysis: If there’s a gap between your costs and available funds, consider different funding options such as seeking investors or taking out a loan.

- Cost Cutting: Alternatively, look for ways to reduce your startup costs by eliminating non-essential expenses or finding cheaper alternatives.

Allocate Funds and Set Budget Limits

With a clear understanding of your costs and available funds, allocate funds to different expense categories and set budget limits.

- Flexible Budgeting: Allocate slightly more funds to categories where costs may fluctuate, such as marketing or inventory.

- Fixed Budgeting: For costs that are fixed, such as rent or insurance, set strict budget limits.

Plan for Contingencies

Finally, it’s vital to include a contingency plan in your budget for unexpected expenses or situations where revenue might be lower than expected.

- Emergency Fund: Include an emergency fund in your budget, consisting of money set aside for unplanned expenses.

- Revenue Shortfall Plans: Develop strategies for scenarios where revenue falls short, such as temporary cost-cutting measures or alternative revenue streams.

Regularly Review and Adjust Your Budget

Remember, a budget is not set in stone. It’s a living document that should be reviewed and adjusted regularly based on your business’s performance and changing circumstances.

- Monthly Reviews: Conduct monthly budget reviews to track your expenses and revenues.

- Adjustments: Based on these reviews, make necessary adjustments to your budget to reflect the realities of your business.

References

[1] Calculate your startup costs

[2] Startup Costs: How Much Cash Will You Need?

[3] How to Determine Your Startup Costs

[4] How to Estimate Startup Costs

[5] Startup Calculator